If you’ve turned on the news lately, it’s hard not to feel like everything is stacking up at once.

Geopolitical conflict is back in the headlines. There is growing chatter around private credit. Markets have pulled back just enough to make people uncomfortable. And layered on top of all of it, we are heading into a midterm election year.

It is the kind of environment that naturally leads to one question:

Should we be doing something different right now?

Before reacting, it is worth stepping back and looking at what has actually happened in environments like this. Every cycle feels unique when you are living through it, but the underlying patterns tend to be more consistent than people expect.

It is also worth remembering what initially rattled markets before geopolitical tensions took over. Fear around AI replacing jobs and disrupting entire industries drove early volatility this year. We saw a rotation out of certain tech and software names as investors questioned whether AI would compress margins or eliminate demand altogether. So far, the data tells a more measured story. We have seen little in the way of productivity gains show up in the data yet, and while hiring has softened, initial jobless claims remain low and unemployment has only ticked up modestly. AI will reshape the workforce over time, but adoption is likely to unfold gradually, not overnight. Like most technological shifts before it, the bigger story is adaptation, not sudden replacement.

WHAT HISTORY SAYS ABOUT CONFLICT AND MARKETS

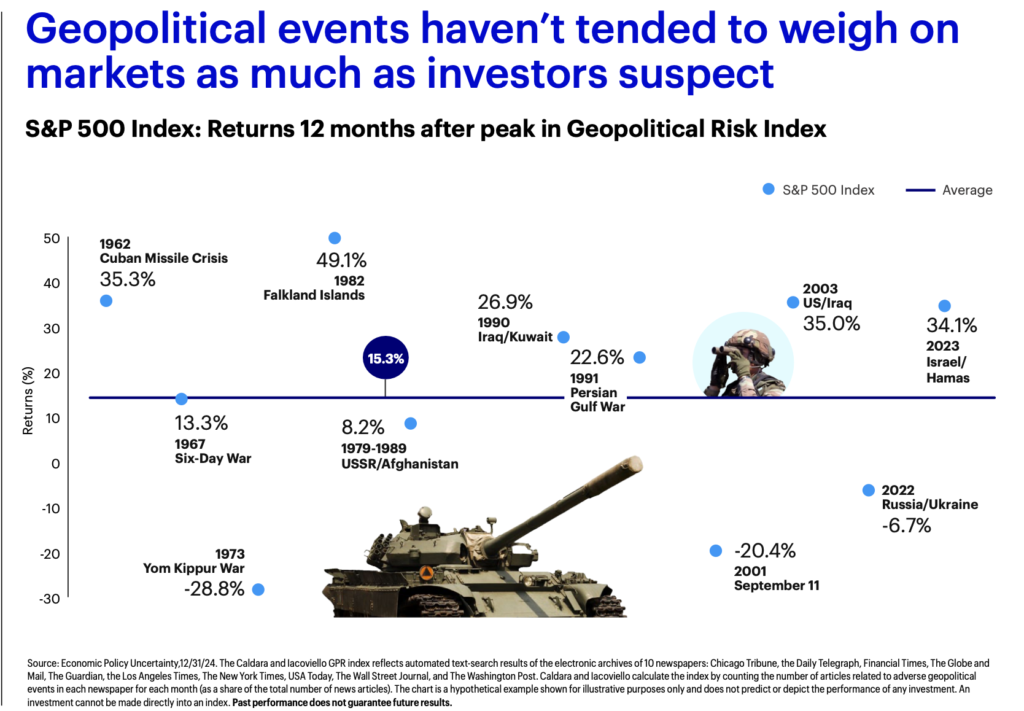

One of the more surprising realities is how resilient markets have been during periods of geopolitical conflict. The human element of war is always shocking and sad, and that is part of why our emotional reaction to these events is so strong, even when markets have not historically responded the same way.

That does not mean markets ignore these events. They do not. Volatility typically increases, and it is common to see short term pullbacks as uncertainty rises. But historically, those drawdowns have been relatively contained and short lived. In many cases, markets bottom within weeks, not months, and are often higher six to twelve months later. This graphic is a great way to visual this, showing S&P returns 12 months after the peak in the Geopolitical Risk Index during different events.

The key distinction is simple. It is not the conflict itself that drives long term market outcomes. It is whether that conflict triggers a broader economic shock.

When wars occur without tipping the economy into recession or disrupting the financial system, markets have generally worked through the uncertainty and moved forward. They are not pricing the headline in front of us. They are pricing the world that comes next.

WHERE THE REAL RISK SITS TODAY

That brings us to the more important conversation right now.

Not the headlines themselves, but what is happening underneath them.

You are starting to see more discussion around stress in private credit markets. Redemption limits, questions around valuations, and a growing realization that liquidity in some of these structures is not what investors assumed it was.

None of this is particularly surprising. Private credit expanded rapidly in a world defined by low interest rates, abundant liquidity, and cheap leverage. That environment allowed a wide range of deals to work. When the cost of capital rises and stays elevated, the math changes.

Borrowers that could comfortably service debt at lower rates now face refinancing at much higher levels. Cash flows get tighter. Margins shrink. Investments that were marketed as stable income can start to show cracks.

The important question is not whether stress exists. It does.

The question is whether it spreads. If a prolonged geopolitical conflict continues to drive up inflation, this could put further stress on credit markets.

So far, that stress appears to be largely contained within private markets. Public credit markets are still functioning. Spreads have moved somewhat, but we have not seen the type of disorderly behavior that typically signals a broader issue.

That distinction matters because markets tend to struggle when financial stress becomes systemic, not simply when it exists.

THE MIDTERM ELECTION DYNAMIC

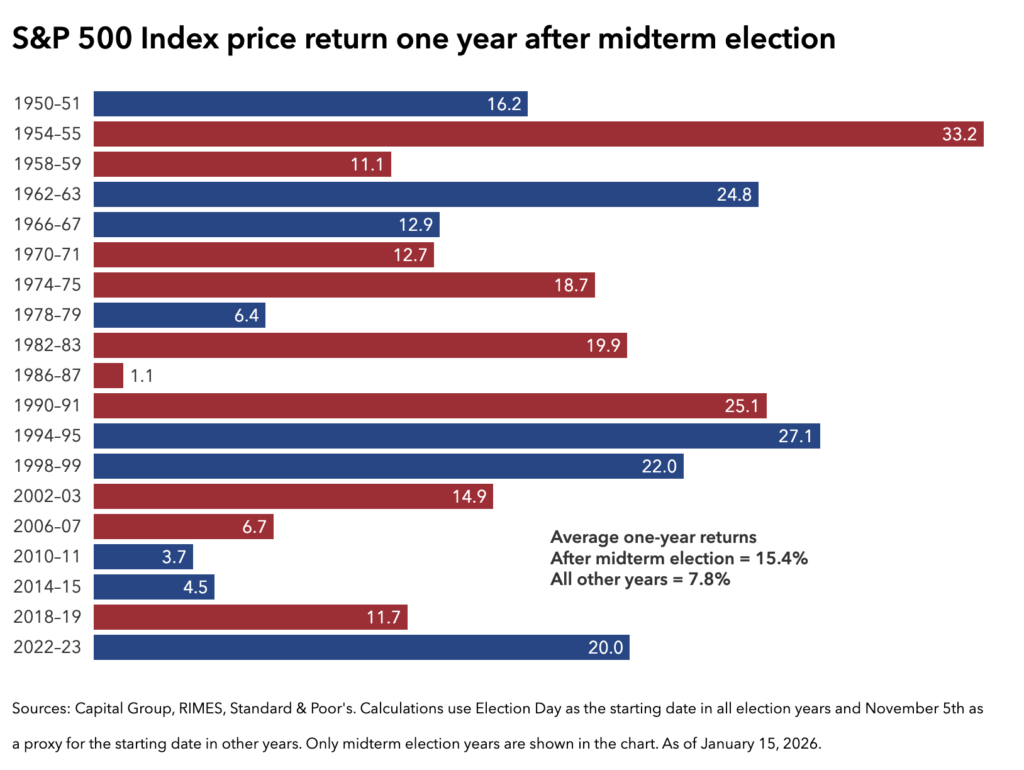

At the same time, we are moving through a midterm election year, which adds another layer of uncertainty.

These years tend to be more volatile, especially in the first half. Markets often struggle to find direction as policy uncertainty builds and sentiment shifts back and forth.

What is less talked about is what tends to happen after.

Historically, the twelve months following midterm elections have been one of the most consistently strong periods for equity markets. Once the election passes, uncertainty begins to clear, policy direction becomes more defined, and markets can reprice forward expectations with more confidence.

The period that feels the most uncertain often sets the stage for stronger forward returns.

CONNECTING WHAT FEELS RISKY AND WHAT ACTUALLY IS

When you step back and connect all of this, the current environment starts to look a little different.

There are real risks. Private credit is something we are watching closely, especially in a higher for longer rate environment. If that stress were to spill into public credit markets, it could have broader implications.

But that is not what we are seeing today.

At the same time, geopolitical conflict is creating noise and short term volatility, but history suggests those events alone rarely derail markets unless they intersect with deeper economic issues. Midterm election years can feel uncomfortable in the moment, but they have often been followed by strong periods for investors.

The challenge is that what feels risky and what has historically been risky are not always the same thing.

WHAT WE ARE FOCUSED ON

In environments like this, it is easy to get pulled into trying to predict what happens next. That is not where we spend our time.

For clients in the accumulation phase, we view periods like this as opportunities to put capital to work at better prices.

For clients who are near or in retirement, we have remained intentionally positioned with a healthy allocation to short term bonds and cash. Not because we can predict when volatility will show up, but because we know that it will.

Different stages, same principle. Stay positioned so no single environment can take you out of the game.

If you have questions about what you are seeing in the headlines or how it connects to your plan, we are always here to talk.