The first half of 2026 has been a good reminder that markets and headlines often tell two very different stories.

Investors have had no shortage of reasons to worry this year. We’ve navigated tariff headlines, geopolitical tensions, fears about AI, concerns around government debt and deficits, questions about the path of interest rates, and a constant debate about whether the economy was finally going to slow down. Yet despite all of that, markets have moved higher.

Even more encouraging, this year’s gains haven’t simply been driven by investors paying higher prices for the same earnings. In many areas of the market, corporate earnings have risen faster than stock prices, causing valuation multiples to actually contract. That’s a healthy setup because, over the long run, earnings drive stock market returns. When profits continue to grow while valuations become more reasonable, it creates a much stronger foundation for future returns than simply relying on investors becoming more optimistic.

THE MARKET HAS BROADENED

Perhaps the most encouraging development of the first half of the year has been the broadening of market performance.

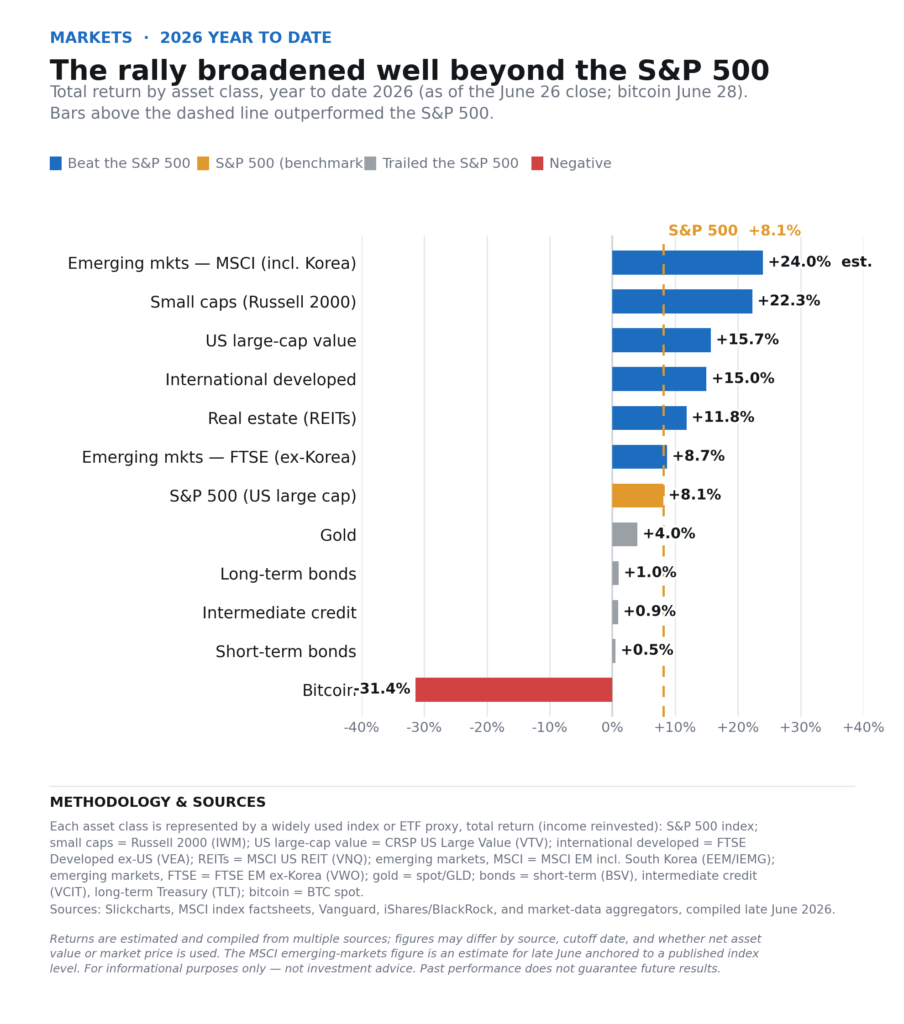

For much of the last several years, it often felt like only a handful of mega-cap technology companies were carrying the market higher. The Magnificent Seven dominated both headlines and returns, and at times it seemed as though diversification was being punished.

This year has looked different.

Performance has broadened beyond the largest growth companies. The S&P 493, equal-weighted indexes, small caps, mid caps, international stocks, and value-oriented areas of the market have all participated more meaningfully. Even with housing in a slump and commercial real estate still recovering, listed real estate (REITs) has been a surprise standout this year, outpacing the S&P 500.

That matters because a market driven by only a few companies can still produce strong returns, but it’s inherently more fragile. A market where gains are being shared across sectors, styles, and regions tends to be healthier and more durable.

It’s also a great reminder of why diversification matters.

Diversification rarely looks brilliant in the moment. There will always be periods when a concentrated bet appears to be the only thing working and investors begin to question why they own anything else. But markets move in cycles. Leadership rotates. It always has and it always will.

This year we’ve already seen significant swings within technology itself. Some of the early AI winners have experienced sharp volatility, while software companies and other areas that lagged in previous years have begun to catch up. The goal isn’t to perfectly predict the next winner. The goal is to build a portfolio that can participate across many different market environments while helping investors stay disciplined through the inevitable changes in leadership.

REASONS TO STAY OPTIMISTIC

As we enter the second half of the year, there are several reasons we’re constructive on the outlook.

Economic growth has remained stronger than many expected, corporate earnings continue to rise, the labor market has remained resilient, and businesses continue to invest in productivity, technology, and innovation. Perhaps most importantly, broader participation has returned to the market. Historically, some of the healthiest bull markets have been the ones where leadership expands beyond a small group of companies.

History also provides an encouraging reminder. While election years can create periods of uncertainty and short-term volatility, every rolling 12-month period following a U.S. midterm election has historically produced positive stock market returns. Past performance never guarantees future results, but it does remind us that periods of political uncertainty have often created opportunities rather than reasons to abandon a long-term plan.

THE BIGGEST RISK IN THE SECOND HALF

While we’re optimistic, we’re not complacent.

The biggest risk we see in the second half of the year is inflation, or more specifically, inflation staying hot enough to keep the Federal Reserve on hold or potentially forcing policymakers to consider another rate hike.

Markets have been supported in part by the belief that the Fed has likely finished raising rates and may eventually be able to lower them. If inflation proves more stubborn than expected, those assumptions could be challenged.

One area we’re watching closely is energy.

If tensions in Iran flare back up and oil prices move sharply higher, that could put renewed upward pressure on inflation at a time when inflation is already running hotter than the Fed would like. Higher energy prices eventually make their way through transportation costs, production costs, and ultimately consumer prices.

That doesn’t mean a recession or bear market is inevitable. It simply means investors should expect the possibility of increased volatility if inflation data disappoints or geopolitical risks push energy prices higher.

Markets can handle uncertainty. What they struggle with most is a meaningful change in expectations. If investors move from expecting future rate cuts to worrying about another rate hike, that could create short-term pressure on both stocks and bonds.

BONDS LOOK DIFFERENT THAN THEY DID IN 2022

One important difference between today and the environment we faced in 2022 is the starting point for bond yields.

In 2022, bonds entered the year with historically low yields, leaving investors with very little income cushion as rates moved sharply higher. Today, yields are starting from a much higher level.

That doesn’t eliminate interest rate risk. If inflation reaccelerates and rates move higher, bond prices could still experience pressure. But higher starting yields help dampen that risk because the income generated from bonds can offset a portion of potential price declines and provides investors with a much healthier starting point than they had several years ago.

For retirees, this is particularly meaningful. For much of the last decade, the conservative portion of a portfolio generated very little income. Today, bonds once again provide meaningful cash flow while also serving as a source of stability and liquidity during periods of stock market volatility.

The fixed income backdrop today is simply healthier than it was in 2022.

THE BIGGER PICTURE

The first half of the year has once again reminded us that successful investing isn’t about predicting every headline. It’s about having a plan and sticking to it.

Markets have risen despite plenty of reasons to worry. Earnings have continued to grow. Performance has broadened. Diversification has worked. And disciplined investors have been rewarded.

Another reason we’re encouraged by the broadening of the market is that the feared economic impact of artificial intelligence has so far been much smaller than many anticipated.

At the beginning of the year, there were widespread concerns that AI would quickly lead to significant job losses and weigh on economic growth. While there has certainly been disruption in some areas, the labor market has remained resilient and the economy has continued to expand.

At the same time, we’re beginning to see something more important. Companies are starting to report tangible benefits from their investments in AI. Productivity improvements, cost savings, and efficiency gains are increasingly showing up in earnings reports and corporate guidance.

In other words, many companies are beginning to capture the benefits of AI before we’ve seen the widespread economic pain that many feared. The first phase of the AI story was concentrated in the companies building the technology. The next phase may belong to the companies using it.

As more businesses adopt AI and begin to realize productivity gains and margin expansion, the benefits could flow to a much wider group of companies and industries. If that happens, it could provide another tailwind for the broadening market participation we’ve already seen this year.

The second half will almost certainly bring periods of volatility. Inflation, interest rates, geopolitical events, and the midterm election cycle will continue to create uncertainty.

But volatility is not the same thing as permanent loss.

For long-term investors, the goal isn’t to avoid every uncomfortable period. The goal is to remain disciplined through them.

We’re constructive, but not complacent.

That means staying diversified, staying invested, and keeping portfolios aligned with goals, time horizon, and risk tolerance. As always, our focus isn’t on predicting every twist and turn in the market. Our focus is helping our clients make wise decisions in the middle of uncertainty and stay invested long enough to benefit from the power of compounding over time.

Disclosure: This article is for informational and educational purposes only and should not be considered investment, tax, or legal advice. All investing involves risk, including the possible loss of principal. Past performance is not indicative of future results, and no investment strategy can guarantee future performance. The views expressed are those of Zizzi Investments as of the date of publication and are subject to change. Advisory services are offered through Zizzi Investments, LLC, a registered investment adviser.