If it feels like everything costs more than it used to, you’re not imagining it.

Inflation over the first half of this decade has already approached, and in some measurements exceeded, the total increase we saw over the entire prior decade.

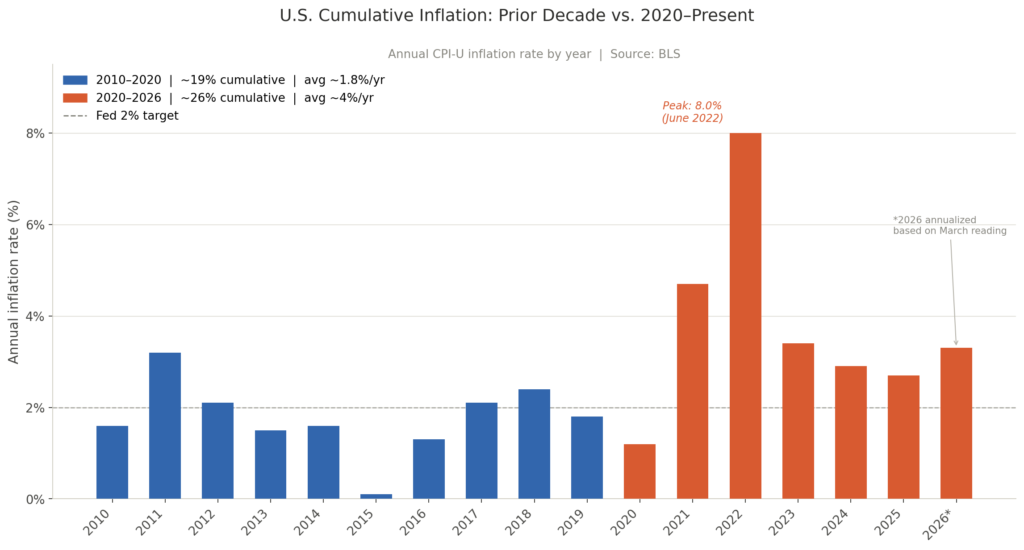

From 2010 through 2019, inflation averaged close to 2% per year. It was a period where price increases felt relatively muted and predictable. Since 2020, that backdrop has shifted. We have experienced multiple years above trend, including the spike above 8% in 2022.

That shift does not just impact what you pay day to day. It shapes how we think about planning, spending, and investing over the long term.

PLANNING FOR REALITY, NOT TARGETS

From the beginning, we have built financial plans at Zizzi Investments using a 3% long-term inflation assumption.

That is slightly above the Federal Reserve’s 2% target, which many planning tools default to. But our goal has never been to anchor to a target. It is to anchor to what we believe is a more realistic long-term environment.

Even a 1% difference in inflation assumptions compounds into a meaningful bridge over time. It impacts retirement income needs, withdrawal sustainability, and how well a plan holds up over decades.

There are also specific areas where we have been even more intentional.

For both healthcare and education, we explicitly model 5% inflation within our plans. This is not a placeholder or a conservative guess. It reflects how these costs have historically behaved relative to overall inflation.

Healthcare and education have consistently trended above headline inflation for decades. Because they represent some of the largest long-term expenses for families, we believe it is important to model them separately and more accurately rather than blending them into a single average.

This approach is not about being overly conservative. It is about building a plan that reflects how costs actually show up in real life.

PUTTING TODAYS INFLATION IN PERSPECTIVE

Using CPI data from the Bureau of Labor Statistics, prices rose roughly 20% over the entire 2010s.

In just the first half of this decade, they have already increased close to 30%, driven largely by the inflation shock in 2022.

Below is a simplified view of that shift.

The key takeaway is not precision to the decimal. It is the pattern.

We have compressed what used to be a decade’s worth of inflation into a much shorter period of time.

WHEN INFLATION BECOMES A PROBLEM

It is easy to assume inflation itself is the issue.

In reality, markets tend to handle inflation better than most people expect. What they struggle with are inflation shocks.

The challenge in 2022 was not just that inflation was high. It was how quickly it accelerated. That rapid change forced equally rapid increases in interest rates, put pressure on both stocks and bonds, and created uncertainty around what comes next.

That is very different from a world where inflation settles into the 3 to 4% range.

In a more stable environment, businesses adjust, consumers adapt, and markets tend to find their footing.

WHY STOCKS STILL PLAY A KEY ROLE

There is a common belief that stocks and inflation do not mix well.

The reality is more nuanced.

Companies are not static. As costs rise, many businesses adjust pricing, improve efficiencies, and work to maintain margins over time. As investors, we participate in that through ownership.

One of the key supports in today’s environment is the overall health of the consumer.

Employment remains strong, wage growth has been solid, and household balance sheets are still in relatively good shape. That gives businesses room to pass through price increases without a significant drop in demand.

Inflation in the 3 to 4% range is not ideal, but it is manageable.

THE RISK THAT DOES NOT MAKE HEADLINES

While market volatility gets most of the attention, the more persistent risk is often quieter.

If inflation is running at 3 to 4% and cash is sitting in a checking account or a low-yield savings account, purchasing power is slowly eroding each year.

It does not feel dramatic in the moment, but over time it adds up.

There is no single solution to inflation. It comes down to thoughtful allocation.

Stocks remain one of the most effective long-term hedges, as companies grow earnings and revenues over time.

Real estate has historically adjusted alongside inflation through both property values and rents.

Gold and alternatives can provide diversification, particularly during periods of uncertainty.

Cash still plays an important role, but it needs to be intentional. When properly allocated in higher-yielding vehicles like money markets or short-term treasury bills, it can help keep pace with current inflation levels. Left idle in traditional bank accounts, it often falls behind, effectively losing purchasing power in today’s environment.

THE BOTTOM LINE

Inflation today is higher than what many people became accustomed to over the past decade, but higher does not mean unmanageable.

What matters most is planning with realistic assumptions, avoiding overreactions to short-term spikes, and staying invested in assets that can grow alongside inflation.

Because at the end of the day, owning productive assets remains one of the most reliable ways to protect and grow purchasing power over time.